The act of ‘buying a cup’ of coffee with crypto is a reality sought by enthusiasts, but checking the BTC price as you leave your house, walking to the coffee shop, and standing in the line hoping the BTC price hasn’t changed before you place your order, is not the ideal way to make a simple purchase.

For money to function optimally it needs to have three basic properties: a medium of exchange, a unit of account, and a store of value. Cryptocurrencies are having major struggles with the last two points. That’s because most cryptocurrencies are deflationary: as the values rise, there are no incentives to spend them on a daily basis.

Cryptocurrencies’ volatility also limits the applications of derivatives, blockchain-based loans, prediction markets, and other longer-term arrangements. All of these challenges have emphasized the need for stable cryptocurrencies, or “stablecoins”.

Stablecoins would offer two main benefits when trading. First, if the market dips they would serve as a safety net. Second, they give those looking for a store of value a clear option for circumventing local banks and collapsing economies. This means people living in countries with unstable economies and harsh political regimes would have an opportunity to access a trusted, censorship-resistant monetary system.

Stablecoins are the obvious route for mainstream adoption. Until they are implemented in a trusted way, however, the crypto economy will remain a sandbox full of bickering geeks. Stability is the backbone of any major corporation, and a breakthrough stablecoin could be the key to changing the crypto landscape and the global economy as a whole.

While searching for an ideal stablecoin we should ask a few questions. Who are the main stakeholders? What kind of stability do we really need? In this article, we will go through the main approaches to creating stablecoins and reflect on the origins of our strive for stability.

Stability is Peace of Mind

Why are we always looking for something stable? Apart from financial incentives, what makes us constantly search for a predictable future?

According to Maslow’s hierarchy of needs, stability and safety overlap to form one of our most basic needs. But we struggle to feel safe on a personal level, let alone financially. Crypto made investing available for everyone, including those with low financial literacy, flooding the market with non-professionals. There is a need for simple instruments to cover risks.

There are no really stable currencies for the time being. USD is definitely not as stable as we used to think. The sheer resources spent on maintaining the dollar’s purchasing power amaze: wars, crimes, bribes, fractional reserve banking, the list goes on…

Perhaps we cannot achieve any stability at all, and continue fooling ourselves, according to Nassim Taleb. This author posited the “black swan” concept, which holds that events are inherently unpredictable. After all, the only value an asset has is the value that the majority of people believe it has. Therefore, most current attempts to create stablecoins could be defined as “faith coins.”

Blockchain has already given us a new understanding of trust, creating incentives for little-known participants to act according to preset rules. This reshapes our relationships with colleagues and higher authority, ultimately unlocking our potential to work across industries, jurisdictions, and countries.

The next generation of stablecoins, based on algorithmically managed supply and demand balance, aims to completely reinvent the global monetary system… but let’s start from the beginning.

In Pursuit of a Stable Currency

It all started back in 2003 with the Linden Dollar, Second Life’s attempt to create a stable internal currency for their virtual world. The Linden Dollar is virtual currency used to buy, sell, rent, or trade land, goods, and services in the virtual universe of Second Life. Linden Dollars can be purchased using US dollars and certain other currencies on the exchange service provided by Linden Lab.

Although it was not by design, the Linden Dollar turned out to be pretty stable. While Linden Dollar has a floating exchange rate against US dollar, the rate has remained between 240 and 270 per $1 over the past decade. You can check out this insightful podcast with the Second Life’s founder Philip Rosedale, explaining their motivation. Recently he came up with another digital universe, this time in VR, with a blockchain-based economy already built in. You can view our full examination of blockchain in the gaming industry.

After the advent of Bitcoin, the first attempt to design stablecoins came from Bitshares back in 2014. It was called BitUSD, and while it was quite stable it failed to achieve mass adoption.

The area became hot property and gained involvement from prominent figures in the industry. To understand it better, though, we should review the main design principles for creating stablecoins.

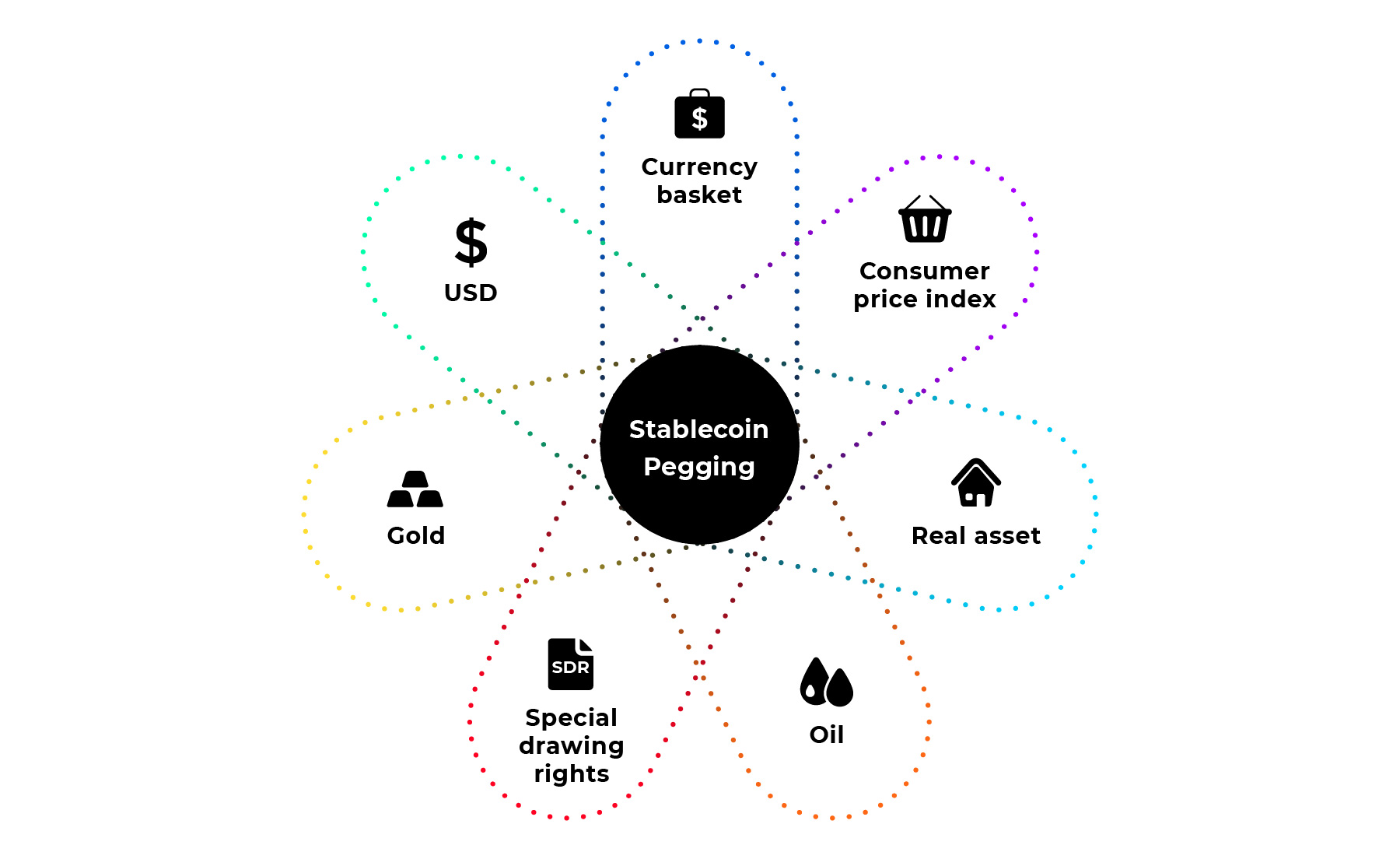

Pegging

Pegging is the most essential element of stablecoins. This is where the currency’s value is tied to another medium of exchange that is considered to be stable.

Stability cannot exist as a pure concept without any reference point. To call a coin stable, we should know the benchmark against which the coin should be stable. It should be “pegged” to some other currency which is considered to be stable. In monetary policy, this is called a fixed exchange rate and there are many examples among national currencies. However, almost all central banks have moved away from currency pegs due to difficulties in maintaining the balance of trade, among other disadvantages. Real-world currency pegs are also expensive to uphold in the long-term, as we can see with the Saudi Arabian Riyal’s troubles being pegged against the US Dollar.  History gives us plenty of evidence that currency pegs cannot withstand black swan events. So it was with the Mexican peso crisis, Black Wednesday, and the Ruble crisis. We can expect it to be the same for the majority of stablecoins in crypto. But before we go too far into this issue with stablecoins, we should make several attempts to create one.

History gives us plenty of evidence that currency pegs cannot withstand black swan events. So it was with the Mexican peso crisis, Black Wednesday, and the Ruble crisis. We can expect it to be the same for the majority of stablecoins in crypto. But before we go too far into this issue with stablecoins, we should make several attempts to create one.

Collateralization

New stable currencies can’t appear out of thin air. No one will support a universal stable currency launched into circulation by another twenty-year-old. Even the USD, though not collateralized by anything other than the authority of US government today, started with a gold standard.

To succeed we should create a collateral for every coin minted, or reassure the whole world in some other way that the currency can be trusted even without the collateral. This can be USD, gold, real-world assets, smart contracts, or another form of trust which can be measured and secured with the newly created currency. But 1:1 collateral sometimes is not enough. If we choose a volatile asset as collateral, such as ETH, we need to cover all possible price drops and fluctuations.

However, if we remember how the gold standard evolved, we would see that 1:1 coverage with gold existed only in the very beginning, gradually decreasing until its complete elimination. Current attempts to create fully collateralized stablecoins resemble the early development stages of any new currency and are dictated by the lack of trust in crypto assets.

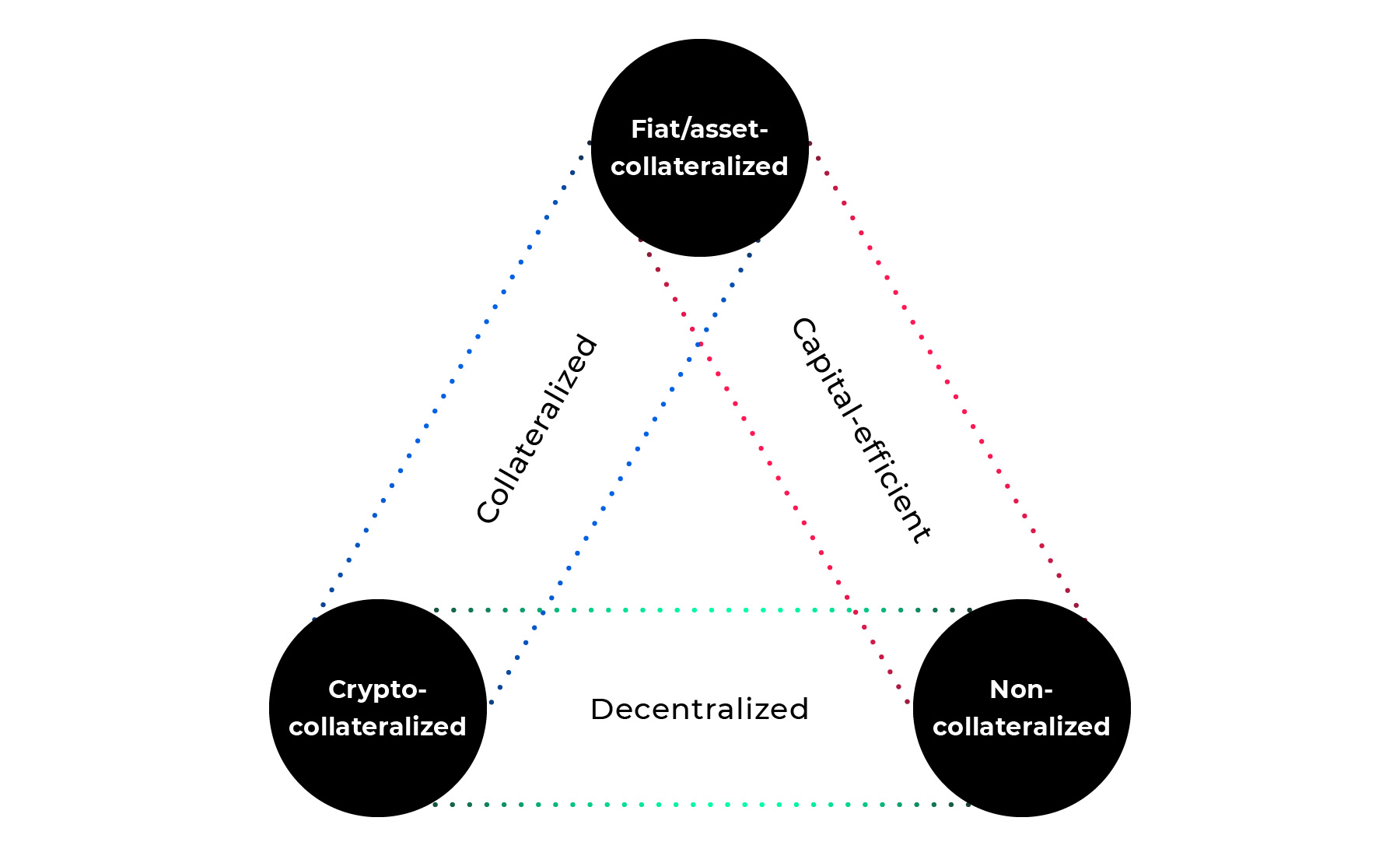

There are three basic approaches.

Fiat/asset-collateralized

These coins are often backed 1:1 by real-world asset like USD, gold, or oil. They are generally very centralized, as the collateral needs to be stored in some trusted environment such as a bank account. The users of a system like this must trust the third party who collateralizes it.

Pros

- Price stability

- Simple logic/low hacking risk (no code involved)

- Free from censorship by governments

Cons

- Require trust in a 3rd party

- Requires expansive audits

- Regulation/hard to receive real USD back due to bank processes

- Pegging to USD might not be stable in the long run

Crypto-collateralized

If we don’t want to depend on the traditional payment infrastructure, we could use crypto assets as collateral. After all, this is cryptoland, so why return to these old banks with their shallow state-backed currencies?

In this case, stability is guaranteed by the crypto asset. In most cases these types of projects mitigate risks by using several currencies, with over-collateralization to cover price volatility. The collateral may be at a ratio of 1:1.5 or more. However, if the collateral drops to zero, it will take the stablecoin with it.

This scheme eliminates the need to trust a third party, but requires economically ineffective over-collateralization, locking up a huge amount of crypto assets.

Pros

- Less centralized

- Can be liquidated cheaply

- Transparency/no audit needed

Cons

- Inefficient use of capital (over-collateralization)

- Can fall to zero during significant price crash

- Complex in design

Non-collateralized

If a crypto-collateralized currency is not enough for a real revolution in the monetary system, why not remove the collateral all together? After all, stability is nothing more than the right combination of supply and demand.

Non-collateralization means that, instead of backing currency with some asset, we create an “algorithmic central bank” managing supply and demand according to rules coded in a smart contract. These coins are also called “fiat stablecoins,” as they work just like the traditional banking system, but in a crypto landscape. If the price goes up, we mint more tokens; if the price goes down, we buy back and burn existing tokens. This is much easier said than done. In the background, non-collateralized stablecoins must have a very complicated design that is still far from perfect.

We could also choose not to peg a coin to the USD, but rather to some economic measures of life stability like the consumer price index (CPI) or special drawing rights (SDR).

With all that mentioned we see non-collateralized stablecoins as the most innovative design solution. These independent stablecoins could not only guard against crypto volatility, but they would also be safeguarded against the collapse of traditional currencies. With the ability to create new stable economics beyond governmental control, non-collateralized stablecoins could become more practical than current fiat currencies and radically change the world. However, there is only room for one solution — all others will likely drop to zero.

Pros

- Decentralized

- No collateral needed

Cons

- Very complex

- High risk of a crash (under some scale)

- Needs future demand for stable coin (continuous growth)

Other approaches

One prominent scheme, proposed by Vitalik Buterin, is to use Collateralized Debt Obligations (CDO) to issue stablecoins against loans with different tranches of seniority. This could be a free market of stablecoins with multiple independent stablecoins competing against each other.

Decentralization

The next important part of stablecoin design is a measure of centralization. Depending on the chosen collateral, we would need to rely on trusted sources. USD should be stored somewhere, such as in a bank, to ensure that it can cover all existing USD-backed tokens in circulation (so this would be a highly centralized version of stablecoin). To mitigate this single-point-of-failure risk, we could peg the stablecoins instead to the basket of national currencies, store collateral in multiple depositories, peg it to more decentralized cryptocurrencies, create hard-coded rules in a smart contract to erase any boundaries, or use a combination of these methods.

Depending on the purpose of the stable cryptocurrency solution we can divide solutions into two categories. The first category aims to combine the current monetary system with crypto assets, adding new instruments on the backbone of existing infrastructure. This would include a USD-pegged stablecoin, which is basically yet another USD derivative used to speculate on the crypto market, rather than to create a stable store of value.

The second category is projects attempting to create an independent monetary system not pegged to any existing currency, but searching for a balance of supply and demand. These approaches are ideologically different, with somewhat controversial outcomes.

The fundamental problem of decentralization in stablecoins is the oracle problem. Blockchains are unable to access data from outside. The price of assets with respect to a stablecoin is external (stored off-chain) data that cannot be available to a price-stabilization smart contract.

There are three fundamental approaches to this problem:

- Trusted data source (oracle).

- Take median of data feeds.

- Use a Schelling point scheme (proposed by Vitalik Buterin).

For a deeper understanding of stablecoins, you can read this fascinating post by Haseeb Qureshi describing all aspects of collateralization and possible design solutions.

The Stablecoin Landscape

Let’s see what’s going on in the stablecoins market, starting with the most straightforward solution: stablecoins backed by fiat or other real-world assets.

The most well-known project is Tether. Tether is a completely centralized solution with USD-backed coins. For now, it’s the most widely used stablecoin with a controversial history involving a Bitfinex/Tether scandal. There are currently $2.6B in Tether tokens in circulation, with no trusted audit on corresponding collateral. The best critique of Tether comes from Bitfinexed, which has been writing specifically on this topic from the very beginning. Despite the centralization and audit issues, Tether remains the best stablecoin in terms of price stability, with no significant drops whatsoever.

The most transparent alternative is presented by TrustToken: the TrueUSD. They positioned themselves as “Tether, but legit”, guaranteed 1 to 1 parity, meaning the token would be redeemable in USD on demand. Tether also guaranteed that at first but later changed their position. TrueUSD has developed a legal framework for collateralized cryptocurrencies with a growing network of compliance and banking partners.

Circle’s USDC is the most well-funded attempt to create a fiat-collateralized stablecoin, and recently raised $110M in Series E investment round. Behind it lies the same idea, but maybe with a better reputation. Circle is a global crypto finance company with multiple products, including the recently acquired Poloniex.

Stably aimed to create transparent reserve-backed stablecoin pegged to USD. This was designed to work across multiple blockchain protocols, including Ethereum and Stellar, using their networks as transparency channels. They are also issuing new tokens via a centralized reserve managed by Stably Inc.

All the projects above are pegged to USD and use it as collateral. AAA Reserve (former Arccy) is not very different in its overall design, but uses multiple sources of collateral including cash, gilts, and AAA-rated credit investments.

DigixDAO is quite different. It’s backed by and pegged to the price of gold. Its stablecoin DGX equals 1 gram of gold. However, they also designed the DGD governance token, which is used for managing the network. While this may look like an excellent solution, the price of gold is not very stable in the long run. In the same vein, we should mention El Petro, which also claims to be a stable cryptocurrency, pegged to oil prices.

Pegging solely to USD is not a very stable solution, especially as crypto is aiming to disrupt numerous traditional industries, banking including. Some projects like Globcoin are linked instead to a basket of several global currencies (15 in this case) and gold. In theory, this could be more resistant to global crises. Globcoin gives the same guarantees as USD-backed stablecoins, and will probably have similar issues with transparency. A similar solution with gold and multiple currencies as collateral comes from X8 Currency.

The question we might ask is, why do we need so much collateralization? The current fractional-reserve banking system has long outgrown this outdated approach of issuing money with 10% collateral at best. This is where Saga comes into the mix. They are the first non-anonymous stablecoin, going against all crypto-libertarian principles. There will be no ICO, so all funds will be raised from accredited investors via private sale. Instead of being pegged to the USD, Saga will be pegged to special drawing rights (SDR) and the token issued by the International Monetary Fund (IMF) tied to an underlying basket of currencies. It will be the first fractional-reserve backed digital currency, aiming at traditional banks. However, it’s still a coin, algorithmically-governed by smart contracts. These contracts will generate SGA tokens on demand and “burn” them if the price spikes.

But the central question remains… who will believe in yet another currency, issued by non-profits, that is not even fully collateralized? So far, Saga has only bigwig advisors to answer this question.

The solution could also come from projects trying to tokenize real assets and supply chains. The Sweetbridge project is working on this by including stablecoin in their economic model. The idea is not to look for the right collateral to back existing currency, but rather to issue new coins based on available world assets of all kinds.

These are the fiat/asset-backed stablecoins. The next category is crypto-collateralized stablecoins backed by crypto assets with a higher degree of decentralization.

The first of these was Bitshares, with BitUSD stablecoin launched in 2014. It’s still tradable, with a roughly $1 exchange rate.

The next big thing was MakerDAO’s Dai, a stablecoin pegged to USD and backed with collateral stored in Ethereum smart contracts. MakerDAO has a flexible price algorithm designed to cover the volatility of crypto collaterals. The project also has a MKR governance token, used to vote for the risk management and business logic of the Maker system.

Boreal is the stablecoin of Aurora Network, a crypto-banking and financial platform. It has a combined collateral of Ether reserves, debt from loans, and DApp endorsements revolving around the IDEX exchange.

Havven is a decentralized payment network and stablecoin that uses a duel-token mechanism. Havven’s token generates collateral via transaction fees collected from users of the network. The second token, Nomins, is a stablecoin used for day-to-day transactions throughout the network. Nomins are backed by Havven tokens, and they can only be issued by locking Havvens into a smart contract.

All these stablecoins rely on some scheme to collateralize them. Preston Byrne offered a reasonable critique of such stablecoins. He suspects that stablecoins are inevitably doomed to fail because even over-collateralized stablecoins would not survive a black swan event.

The following stablecoins are non-collateralized. Instead, they are trying to create an algorithmic central bank for crypto assets.

The Nubits project, started back in 2014, provides a stablecoin (USNBT) pegged to the US dollar. Apart from this, they planned to have multiple stablecoins pegged to other global currencies. NuBits must be one of the first algorithmically-managed stablecoin in crypto. Its price was stable for more than 3 years but recently dropped into a death spiral.

The most prominent project in this field is Basis (former BaseCoin), which recently raised $133M from the likes of A16z and Google Ventures. Basis presented itself as a stable cryptocurrency with an algorithmic central bank. When demand is rising, the blockchain will create more Basis. The expanded supply is designed to bring the Basis price back down. When demand is falling, the blockchain will buy back Basis to restore price. However, it’s not as simple as it seems. They have a token economy based on three different tokens (Base coin, bonds, and shares), all enforced by smart contracts. A detailed explanation can be found in the Basis whitepaper.

The main problem here is that this model relies on continual growth of the system to cover price gaps. Basis plans to stimulate this process with the infusion of funds they’ve raised until the network gains a critical mass. But would this be enough?

There are several other projects in the area working on similar principles like Fragments, Carbon, Kowala, and Minexcoin. All of these are non-collateralized stablecoins pegged to the USD dollar.

| Fiat/asset-collateralized | Crypto-collateralized | Non-collateralized |

| Tether | BitUSD | Basis |

| TrueUSD | DAI (MakerDAO) | Fragments |

| USDC (Circle) | Boreal | Carbon |

| Stably | Havven | Kowala |

| AAA Reserve (fmr. Arccy) | Nubits | Minexcoin |

| Globcoin | ||

| DigixDAO | ||

| X8 Currency | ||

| Saga | ||

| Sweetbridge |

Future governments

Non-collateralized stablecoins are really what all crypto-anarchists are praying for, since most governments today control their money supply, thereby controlling citizens by limiting purchasing power. What if the money became independent from governments? Individuals may become more sovereign and empowered by the freedom of decentralization. Governments in their current form may become obsolete, and would forced to drastically change their policies and legislation.

A lot of millennials are seeking non-traditional banking services like Venmo, the mobile payment service with a world-class user experience. Developing countries are cut off from banking due to the banks’ “de-risking” policies. State efforts to create “”national crypto” are miserable, indicating a lack of instruments to control the upcoming wave of independent currencies.

Stablecoins could create independent money and tax revenues flow. Of course, governments are still needed at least to create infrastructure, but for some countries, censorship-resistant money would offer a way to survive the enormous changes of national currencies. Stablecoins could introduce a new level of trust as people around the world choose in favour of a global currency instead of their local regime.

Conclusion

Achieving stability is one of our basic needs, both as individuals and as economic actors. Without a stable currency in the crypto economy, there will be little incentives to spend rather than HODL.

In the current landscape of stablecoin solutions, we can see similar patterns to traditional monetary systems. It seems like stablecoins would pave the way from asset-backed options to algorithmic solutions, mirroring the dollar’s shift away from the gold standard. If stablecoin solutions succeed, they could replace the current monetary system, radically transforming the world’s economy.

Creating and maintaining stability in this chaotic political and economic climate seem just out of reach. Our solutions, not to mention our mental ability to process all this information, are likely to be a few steps behind the increasing complexity of the world, so we may not like the ultimate answer to the price-stability question.

It could be better to wait for cryptocurrency to reach maturity and see how it can interact with traditional instruments before trying to create a change-the-world stablecoin. Ultimately we may find that the Holy Grail we are all searching for is buried in a different field…